What I Learned About Money When the Unexpected Hit

I never thought I’d be one of those people caught off guard by a sudden expense—until I was. A broken-down car, a surprise medical bill, and then my fridge gave up the ghost. That’s when I realized: knowing how to spot financial risks before they explode is just as important as saving money. This is what I discovered while figuring out how to protect myself, not just recover. If you’ve ever felt unprepared, you’re not alone—and there’s a way forward. It’s not about having a perfect budget or a six-figure income. It’s about seeing what could go wrong before it does and building quiet strength beneath the surface of everyday life. The peace that comes from preparedness is worth more than any windfall.

The Wake-Up Call: When Life Throws a Curveball

It started quietly. One morning, the car wouldn’t start. The mechanic’s estimate came in at over $900—a sum that didn’t exist in the checking account. Two weeks later, a routine doctor’s visit led to a follow-up test, then a bill for nearly $1,200. Insurance covered part, but the rest landed like a stone in the pit of the stomach. Then, just as the calendar turned, the refrigerator stopped cooling. Groceries spoiled overnight. The replacement cost? Another $1,000, not including delivery. These weren’t luxury purchases or careless spending. They were unavoidable, necessary expenses—each small in isolation, but together, they cracked the foundation of financial stability.

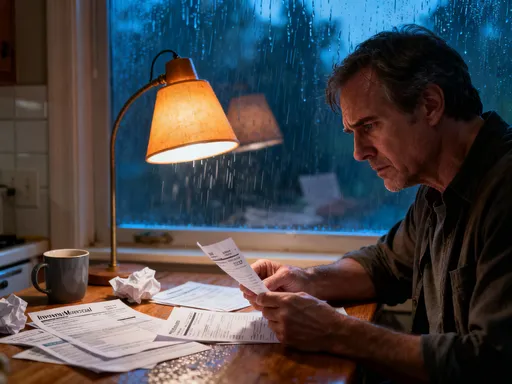

The emotional toll was just as heavy as the financial one. There was no single moment of crisis, but a slow erosion of confidence. Sleep became harder. Decisions felt heavier. The simple act of checking the bank balance brought dread instead of reassurance. The worst part wasn’t the money lost—it was the helplessness. It felt like being caught in a storm without an umbrella, watching each new downpour soak through. This wasn’t poverty, but it wasn’t security either. It was the fragile middle ground where most families live—just one or two steps from real trouble. And it revealed a truth many avoid: financial stability isn’t just about income or savings. It’s about resilience. It’s about how well you can absorb the shocks life inevitably delivers.

What made it worse was the timing. These events didn’t happen over years. They came within weeks. There was no time to adjust, no chance to rebuild between hits. That’s when it became clear: traditional money advice wasn’t enough. Saving 20% of income or cutting out lattes wouldn’t have prevented this. Those tips assume a steady path. But real life isn’t steady. It’s unpredictable. The flaw wasn’t in the effort—it was in the focus. Too much attention had gone to growing money, not enough to protecting it. The goal had been accumulation, not preservation. And in that imbalance lay the real danger. The lesson wasn’t to save more in the moment of crisis. It was to see the risk before the moment ever arrived.

Why Risk Identification Beats Quick Fixes

When a financial emergency strikes, the instinct is to fix it fast. Pay with a credit card. Take out a short-term loan. Borrow from family. These solutions offer immediate relief, but they often deepen the problem. A $900 car repair charged to a card at 19% interest can grow into $1,100 over a year. A payday loan for a medical bill might come with fees that double the original amount. These aren’t solutions—they’re transfers of pain, pushing the burden into the future. The real win isn’t in reacting quickly. It’s in not having to react at all.

Consider two people facing the same car breakdown. One has a fund set aside for irregular expenses. The repair is handled with cash, no debt, no stress. The other charges it, then struggles for months to make minimum payments, accruing interest and late fees. Both spend the same on repairs, but their outcomes diverge sharply. The first preserves stability. The second risks a spiral. The difference isn’t income. It’s preparation. It’s the ability to identify risks before they become emergencies. This kind of foresight doesn’t require complex investing or market timing. It starts with asking simple questions: What could go wrong? How would I pay for it? What would happen if I lost my job tomorrow?

Yet most people avoid these questions. Denial is a powerful force. It’s easier to believe that bad things won’t happen than to face the effort of preparing for them. Overconfidence plays a role too. Many assume their job is secure, their health is fine, their car is reliable—until one isn’t. There’s also a cultural bias toward optimism. Talking about risk feels negative, even defeatist. But in finance, realism isn’t pessimism. It’s responsibility. The most dangerous financial belief isn’t greed. It’s the assumption that stability is permanent. Risk identification flips the script. Instead of chasing high returns, it focuses on avoiding big losses. And in the long run, avoiding a single major financial setback can do more for your net worth than years of aggressive investing.

The Hidden Risks Everyone Ignores

Most people think of financial risk as market crashes or job loss. But the real threats often come from quieter, less visible sources. One of the most common is job dependency—the reliance on a single income stream. For many families, the loss of one paycheck would mean immediate hardship. Yet few have a plan for it. Another overlooked risk is insurance gaps. Homeowners may not realize their policy doesn’t cover water damage from a burst pipe. Renters might assume their landlord’s insurance protects their belongings—when it doesn’t. These gaps don’t matter until they do, and when they do, the cost can be devastating.

Digital fraud is another growing threat, especially during times of stress. A single phishing email, clicked in a moment of distraction, can lead to unauthorized transactions, drained accounts, or identity theft. The risk isn’t just from hackers overseas. It’s from the small lapses in daily habits—using weak passwords, sharing too much on social media, or skipping software updates. Emotional spending is another silent danger. When under pressure, many turn to retail therapy. A $200 online purchase might feel like relief in the moment, but it weakens the financial buffer just when it’s needed most. These behaviors don’t show up on a balance sheet, but they erode resilience over time.

What makes these risks so dangerous is their invisibility. They don’t announce themselves. They grow in the background, unnoticed until they erupt. A layoff exposes the lack of emergency savings. A scam reveals poor digital hygiene. A medical emergency uncovers insurance flaws. The lesson isn’t to live in fear. It’s to shine a light on the shadows. By naming these risks, we take away their power. We shift from passive victims to active protectors. And that shift begins with awareness—recognizing that risk isn’t just about big disasters. It’s in the small, everyday oversights that compound into crisis.

Building Your Early Warning System

Just as a smoke detector alerts you to fire before it spreads, a financial early warning system helps you catch problems before they grow. The first step is tracking irregular expenses. Most budgets focus on rent, groceries, and utilities—predictable costs. But the real strain often comes from the unpredictable: car repairs, pet emergencies, school fees. Start by reviewing the last 12 months of bank statements. Flag every non-monthly expense over $100. Add them up. Divide by 12. That number is your true monthly cost for irregular items. Set up a separate savings account and automate a transfer each month to cover it. This isn’t a luxury. It’s a buffer against surprise.

The second part of the system is monitoring cash flow. A sudden drop in income—due to reduced hours, a missed freelance job, or a family obligation—can signal trouble ahead. Track your net income weekly, not just monthly. If it dips two months in a row, treat it as a red flag. Ask: Is this temporary? What would happen if it continued? Could bills still be paid? The third element is vulnerability assessment. Once a quarter, sit down and ask a series of questions: What would happen if I lost my job? What if a family member got sick? What if my car broke down? Be specific. Estimate the costs. Note the gaps in coverage. This isn’t about fear. It’s about clarity. Over time, this practice builds a mental map of risk—your personal financial radar.

The goal isn’t perfection. It’s pattern recognition. You’re not trying to predict every disaster. You’re learning to spot the early signs of strain. A late utility payment. A growing credit card balance. A skipped savings transfer. These are not just mistakes. They’re signals. They tell you when your system is under pressure. And when you see them early, you can adjust—reduce spending, increase income, or tap a reserve—before the situation worsens. This kind of awareness turns financial management from a reactive chore into a proactive habit. It’s the difference between being blindsided and being ready.

How Small Habits Defuse Big Threats

Resilience isn’t built in a day. It’s grown through small, consistent actions. One of the most effective habits is reviewing bank and credit card statements weekly. It takes less than ten minutes. The goal isn’t just to track spending. It’s to catch errors, spot unfamiliar charges, and notice patterns. A $50 subscription you forgot to cancel. A duplicate payment. A merchant charging more than expected. These aren’t major losses on their own, but they add up. More importantly, they train your eye to see anomalies—early signs of fraud or mismanagement.

Another powerful habit is setting up transaction alerts. Most banks allow you to receive a text or email when a charge exceeds a certain amount—say, $100. This simple feature can stop a stolen card from being drained. It also creates awareness of large outflows, helping you stay within budget. A third habit is the quarterly money check-in. Set a calendar reminder every three months. Use it to review your budget, update your emergency fund balance, check insurance coverage, and reassess your risk map. This isn’t a deep audit. It’s a tune-up—a chance to make small adjustments before big problems arise.

These habits work because they’re low-effort and high-leverage. They don’t require financial expertise. They don’t take hours. But over time, they build a layer of protection. Weekly reviews catch problems early. Alerts provide real-time feedback. Quarterly check-ins ensure long-term alignment. Together, they form a rhythm of awareness. And that rhythm changes your relationship with money. Instead of feeling out of control, you feel informed. Instead of reacting to crises, you anticipate them. The power isn’t in any single action. It’s in the repetition. Like brushing your teeth, these habits prevent decay—not of enamel, but of financial health.

Tools That Help Without Overcomplicating

Technology can support these habits, but only if used wisely. Budgeting apps, for example, can automate expense tracking, categorize spending, and show trends over time. The best ones sync with bank accounts, update in real time, and send alerts when you’re near a limit. They turn abstract numbers into visual patterns—making it easier to spot overspending in dining out or subscription services. But the goal isn’t to track every penny. It’s to see the big picture. A simple bar chart showing rising utility costs can prompt a conversation about energy efficiency. A spike in grocery spending might lead to better meal planning.

Automated savings tools are another helpful resource. Many banks allow you to set up recurring transfers to a separate account—labeled for emergencies, car repairs, or medical costs. Some apps even analyze your spending and save small amounts automatically when you’re under budget. These tools remove willpower from the equation. They make saving invisible, which makes it sustainable. Credit monitoring services add another layer. They alert you to changes in your credit report, new accounts opened in your name, or inquiries you didn’t authorize. This isn’t just for fraud prevention. It’s for peace of mind. Knowing your credit is secure reduces background anxiety.

But tools have limits. The danger isn’t in using them. It’s in overusing them. Some people jump from app to app, chasing the perfect system. They spend more time managing tools than managing money. This is called analysis paralysis—the illusion of progress without real action. The key is simplicity. Choose one or two tools that fit your lifestyle. Use them consistently. Ignore the rest. A basic spreadsheet, a single budgeting app, and automatic transfers can do more than a dozen complex platforms used inconsistently. Technology should serve you, not distract you. When used with purpose, it becomes an ally in risk awareness—helping you see, act, and stay ahead.

From Panic to Prepared: A Mindset Shift

The journey from financial stress to confidence isn’t about reaching a specific dollar amount. It’s about changing how you think. At first, the focus is on loss—what could go wrong, what might be taken away. But over time, that shifts. Preparedness becomes a source of strength, not fear. The same person who once panicked at a $300 bill now handles a $1,200 expense with calm. Not because the money is easy to find, but because the plan is already in place. The emergency fund covers it. The insurance claim is filed. The budget adjusts. There’s no drama. There’s only action.

This mindset isn’t built overnight. It grows from repeated practice—from asking the hard questions, building the habits, using the tools, and learning from small setbacks. Each time you catch a problem early, you reinforce the belief that you’re in control. Each time you avoid a debt spiral, you gain confidence. The emotional payoff is profound. Anxiety fades. Sleep improves. Decisions feel lighter. You stop living in reaction mode and start living with intention. Money becomes less of a source of stress and more of a tool for stability.

Looking back, the broken car, the medical bill, the dead fridge—they weren’t just setbacks. They were teachers. They revealed the gaps in awareness, the blind spots in planning, the cost of ignoring risk. But they also opened a path forward. The same lessons can be learned without the pain—by choosing to see, to prepare, to act. Financial security isn’t about perfection. It’s about progress. It’s about knowing you’re not invincible, but you’re not helpless either. And in that balance lies true peace of mind.